FMLA vs. Short-Term Disability: Which Do You Need?

Last updated:

When a serious health condition forces you to take time off work, two options come up again and again: FMLA and short-term disability. They sound similar. People use them interchangeably. But they do very different things, and confusing the two could cost you either your paycheck or your job.

Here’s the quick version: the Family and Medical Leave Act (FMLA) protects your job. Short-term disability insurance (STD) replaces part of your income. And in many cases, you can use both at the same time. This guide breaks down exactly how FMLA vs. STD works, who qualifies, and how to get the documentation you need fast.

What Is FMLA and How Does It Protect Your Job?

The Family and Medical Leave Act (FMLA) is a federal law that provides eligible employees with up to 12 weeks of unpaid, job-protected leave in a 12-month period. Congress passed FMLA in 1993, and the U.S. Department of Labor administers the program. The key benefit is job protection: your employer can’t fire you, demote you, or replace you for taking FMLA leave.

FMLA covers a broad range of qualifying reasons, including:

-

Your own serious health condition (surgery recovery, cancer, chronic pain, anxiety, depression)

-

Caring for a spouse, child, or parent with a serious medical condition

-

Bonding with a newborn, adopted, or foster child

-

Qualifying situations related to a family member’s military service

-

Up to 26 weeks of leave to care for a covered servicemember with a serious injury

Not every employee is eligible, though. To qualify for family and medical leave under FMLA, you must meet these requirements:

-

Worked for a covered employer for at least 12 months

-

Logged at least 1,250 hours during that 12-month period

-

Work at a location where the employer has 50 or more employees within 75 miles

Covered employers include all public agencies, public and private elementary and secondary schools, and private companies with 50+ employees. Your employer must also continue your health insurance coverage during FMLA leave under the same terms as if you were still working.

The catch? FMLA leave is unpaid. You get job protection, not a paycheck. That’s where short-term disability comes in.

What Is Short-Term Disability Insurance?

Short-term disability (STD) is an insurance benefit that replaces a portion of your income when a medical condition prevents you from working. Unlike FMLA, STD operates as an insurance product, either provided by your employer or purchased on your own.

Key details about short-term disability insurance:

-

Income replacement: Typically pays 40-70% of your regular salary

-

Duration: Benefits last anywhere from a few weeks to 26 weeks (6 months), depending on the policy

-

Waiting period: Most policies have a 7-to-30-day elimination period before benefits begin

-

Coverage scope: Only covers the employee’s own medical condition (not caregiving or family bonding)

-

Job protection: STD does not guarantee your job will be held for you

On a federal level, employers are not required to offer short-term disability insurance. However, several states have leave laws that mandate some form of disability coverage: California, Hawaii, New Jersey, New York, and Rhode Island (Puerto Rico also requires it). If you don’t live in one of those states, coverage depends entirely on your employer’s benefits package.

You should also know what STD doesn’t cover. If you need time off to care for a family member, bond with a new child, or deal with a non-medical family situation, short-term disability won’t apply. Those scenarios fall under FMLA.

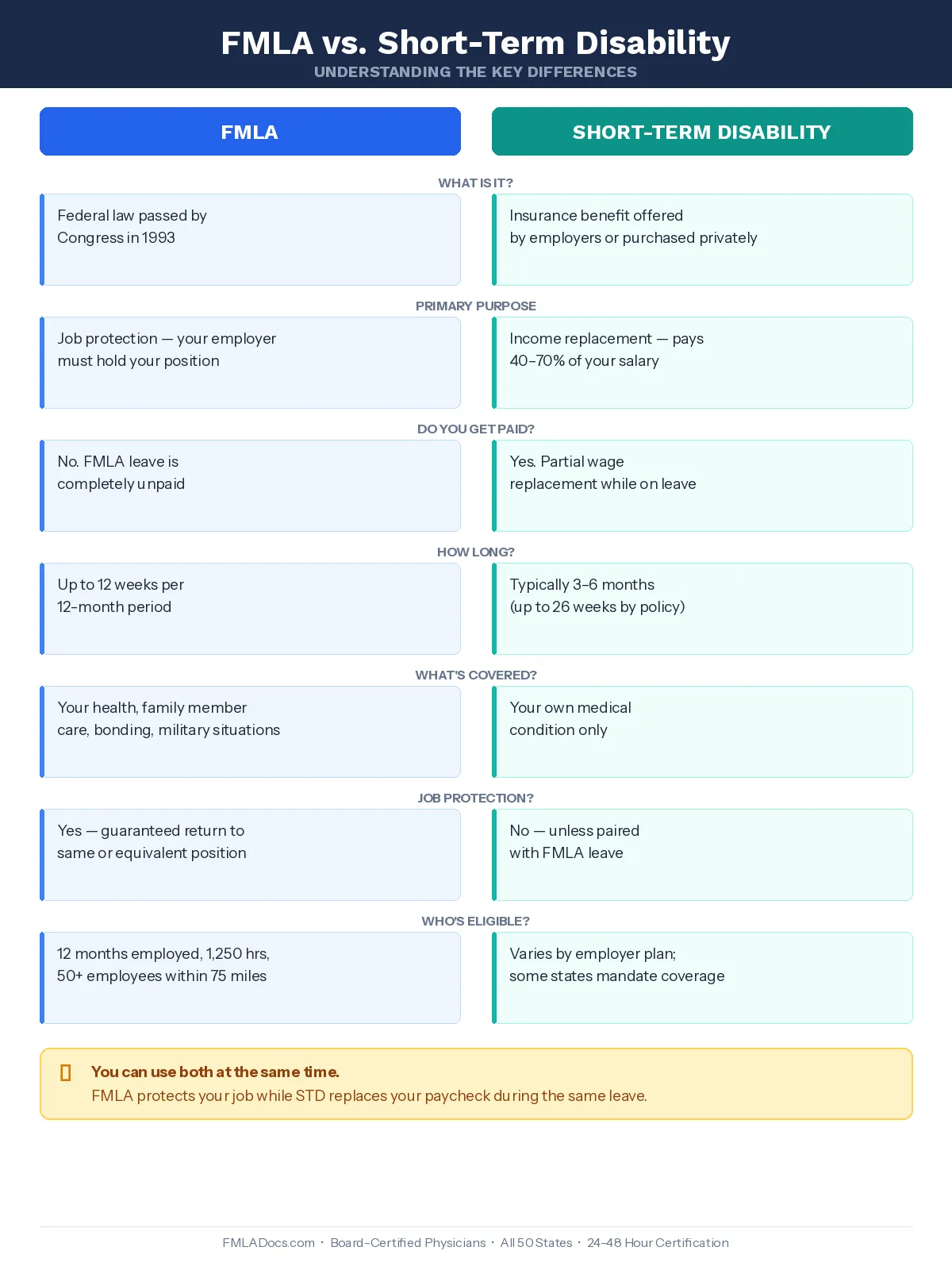

FMLA vs. Short-Term Disability: Key Differences

When comparing FMLA vs. short-term disability, the simplest way to think about it is this: FMLA is a legal protection, and STD is a financial benefit. They address two completely different problems, which is why they work so well together.

Other key differences between FMLA vs. STD:

-

FMLA requires employers to restore you to the same or an equivalent position. STD has no such requirement.

-

FMLA allows intermittent leave (taking time off in smaller blocks). Most STD policies require continuous leave.

-

Employees are eligible for FMLA only after meeting strict federal criteria. STD eligibility varies by plan and may start on day one of employment.

-

FMLA applies to all covered employers regardless of whether they offer insurance. STD is only available if your employer offers it or you purchase a policy.

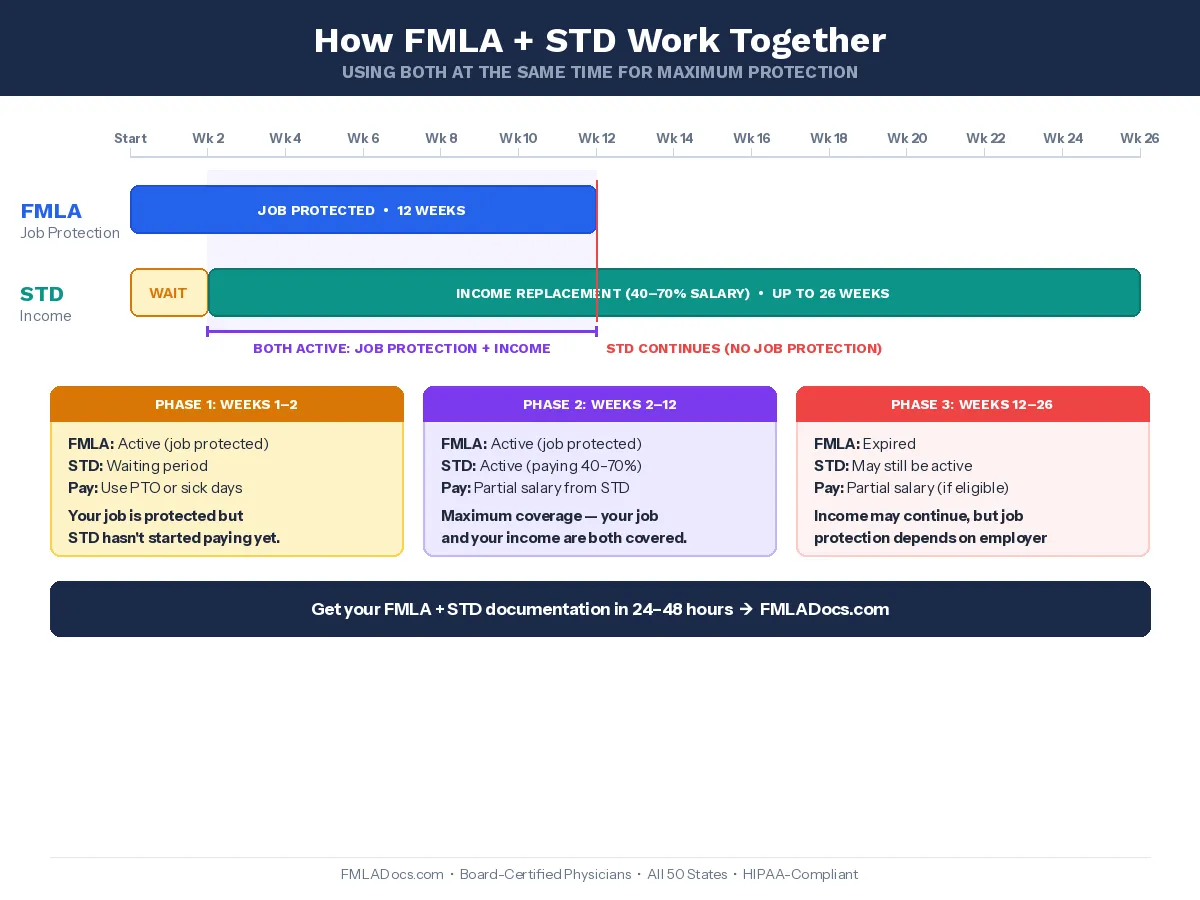

Can You Use FMLA and Short-Term Disability Together?

Yes, and this is the most important thing to understand about FMLA vs. short-term disability. When you qualify for both, they run concurrently. FMLA protects your job while STD replaces part of your paycheck during the same leave period.

Here’s how the timeline typically works:

-

Day 1: Your medical leave begins. FMLA leave starts, and your 12-week clock begins ticking.

-

Days 1-14: You’re in the STD waiting/elimination period. You may use PTO or sick days.

-

Week 2-12: Short-term disability benefits kick in, paying 40-70% of your salary. FMLA continues running.

-

After week 12: FMLA job protection ends. STD benefits may continue for several more weeks depending on your policy, but your employer is no longer legally required to hold your position.

What happens after FMLA runs out is a common concern. If your short-term disability insurance extends beyond 12 weeks, you can still receive income replacement. However, without FMLA, your job protection depends on your employer’s policies, state leave laws, or potential protections under the Americans with Disabilities Act (ADA).

The bottom line: if you qualify for both, use them together. You don’t have to choose one or the other.

Which One Do You Need? Common Scenarios

The right approach depends on your situation. Here’s how FMLA vs. STD typically applies across the most common medical leave scenarios.

Mental Health Conditions

Conditions like anxiety, depression, PTSD, panic disorder, and severe burnout can qualify for both FMLA and short-term disability. FMLA protects your position while you pursue treatment. If your STD policy covers mental health (most do), you receive income replacement at the same time.

-

Your employer cannot ask for your specific diagnosis under FMLA

-

A medical leave request for mental health is treated the same as any other serious health condition

-

FMLA for anxiety and depression is one of the most common reasons employees take medical leave

Pregnancy and Maternity Leave

Short-term disability typically covers 6-8 weeks of medical recovery after childbirth. FMLA covers the full 12 weeks, including bonding time. Used together:

-

STD pays partial income during the recovery period

-

FMLA protects your job for the full 12 weeks

-

Remaining FMLA weeks after STD ends provide unpaid, job-protected bonding time

-

State paid family leave programs may provide additional coverage

Getting your FMLA certification for pregnancy before your due date helps avoid last-minute paperwork stress.

Chronic Conditions and Surgery

For ongoing conditions like fibromyalgia, diabetes, migraines, or back problems, intermittent FMLA allows you to take leave in smaller blocks for flare-ups and appointments. For scheduled surgeries:

-

File FMLA paperwork before your surgery date

-

STD benefits cover income during recovery

-

FMLA holds your position while you heal

-

If recovery takes longer than expected, STD may extend beyond the FMLA period

How to Get Your FMLA and STD Documentation

Both FMLA and short-term disability require medical certification from a licensed healthcare provider. For FMLA, your employer will supply a certification form (typically the DOL’s WH-380 form). For STD, your insurance carrier has its own documentation requirements.

The traditional process can be slow:

-

Schedule a doctor’s appointment (wait days or weeks)

-

Sit through the visit

-

Wait for the office to complete paperwork

-

Follow up on missing information

-

Back-and-forth between your doctor, employer, and insurance company

Through FMLADocs, you can get your FMLA certification and short-term disability documentation completed in 24-48 hours via a telehealth consultation with board-certified physicians licensed in all 50 states. Everything stays HIPAA-compliant and confidential, and employers nationwide accept the documentation.

| Factor | Online Certification (FMLADocs) | Traditional Doctor Visit |

|---|---|---|

| Time | 24-48 hours | 1-3 weeks |

| Cost | Affordable flat rate | $100-$300+ |

| Convenience | From home, any time | Office hours only |

| Employer Acceptance | All 50 states | Yes |

| Follow-Up | Included | Additional visit needed |

Take the Next Step

Understanding the difference between FMLA vs. short-term disability puts you in control of your leave options. FMLA is your job protection. Short-term disability insurance is your income replacement. Used together, they give you the strongest safety net available under federal law.

If you’re dealing with a serious health condition, preparing for surgery, managing a mental health crisis, expecting a baby, or caring for a family member, you don’t have to navigate this alone. FMLADocs connects you with board-certified physicians who can complete your FMLA certification and short-term disability documentation in 24-48 hours, accepted by employers in all 50 states.

Frequently Asked Questions

Can you use FMLA and short-term disability at the same time?

Yes. When employees are eligible for both, FMLA and short-term disability typically run concurrently. FMLA provides job protection while STD provides partial income replacement during the same leave period. This gives you financial support and the legal guarantee that your employer must hold your position.

Is short-term disability the same as FMLA?

No. The core distinction when comparing FMLA vs. short-term disability is that FMLA is a federal law providing unpaid, job-protected leave for qualifying medical and family reasons, while short-term disability is an insurance benefit that replaces a portion of your income during a medical absence. They serve different purposes and operate under different rules, but they can work together.

Does FMLA pay you while you're off work?

No. FMLA leave is unpaid. However, your employer must continue your health insurance during FMLA leave. You can apply accrued PTO concurrently with FMLA, and short-term disability insurance can replace part of your income while FMLA keeps your job secure.

What happens when FMLA runs out but STD continues?

After 12 weeks, FMLA job protection ends. If your short-term disability policy provides benefits beyond that point, you'll continue receiving income replacement, but your employer is no longer federally required to hold your job. State laws, company policies, or the ADA may offer additional protections depending on your situation.

Can you be fired while on FMLA leave?

No. A covered employer cannot legally terminate, demote, or retaliate against an employee for taking FMLA leave. You have the right to return to the same or an equivalent position. However, if the company would have eliminated your role regardless of your leave (e.g., during a company-wide layoff), the employer does not have to create a new role for you.

Meet the author

Alisha Shabbir

Alisha is a health content specialist with 7 years of experience writing about employee benefits, medical leave, and healthcare access. With a background in healthcare communications, she breaks down complex regulations and medical topics into practical, actionable guidelines. From workplace wellness to preventive health, she helps readers navigate the healthcare system with confidence. When she's not working, she enjoys long walks, baking, and spending time with her pets.

Get Your FMLA Certification Online in Minutes

Start Now